Mastering Your Budget A Step-by-Step Guide on How to Manage Personal Finances Effectively

Finance

|

March 27, 2026

In today’s economic environment, many individuals are facing increased pressure on their personal finances due to rising living costs, higher interest rates, and growing debt obligations. Everyday expenses such as housing, transportation, and credit card payments are taking up a larger share of monthly income, leaving less room for savings or long-term planning.

In today’s economic environment, many individuals are facing increased pressure on their personal finances due to rising living costs, higher interest rates, and growing debt obligations. Everyday expenses such as housing, transportation, and credit card payments are taking up a larger share of monthly income, leaving less room for savings or long-term planning.

As a result, many people struggle not only with managing day-to-day budgets but also with reducing debt and building financial stability for the future. This makes understanding personal finance principles and making informed financial decisions more important than ever.

Learning to manage finances proficiently is crucial for achieving monetary stability and fostering a sense of emotional well-being. By gaining skills in budgeting, responsible spending, and strategic saving, individuals can alter their financial narratives and strive towards an economically secure future. Navigating these complexities empowers readers to take control of their financial situations, paving the way for better expense management and preparation for unforeseen challenges. The strategies included in this guide will unveil actionable insights and tools that lead to financial empowerment and enhanced life quality.

Understanding Personal Finance Management

Managing personal finances is fundamentally the process of budgeting, saving, investing, and analyzing one’s financial activities to ensure clarity in achieving financial goals. At its essence, personal finance management strives to build a solid financial foundation that supports day-to-day life, encompassing everything from bill payments to rigorous planning for retirement and unforeseen emergencies.

Cultivating strong financial habits is essential for enduring stability. These habits involve meticulously tracking expenses, developing a budget that faithfully reflects one’s income and spending priorities, and committing specific portions of funds to savings and investments. This strong grasp of personal finance not only enhances one’s capability to make informed decisions but also alleviates the stress linked to financial uncertainties.

Furthermore, effective financial management bestows independence and security upon individuals. It enables informed choices regarding spending, consumption, and savings, ultimately fostering a comfortable lifestyle and the resilience needed to handle unexpected financial hurdles. In a world where financial demands can arise unexpectedly, honing robust financial habits transcends mere capability—it becomes an indispensable skill necessary for navigating daily existence while securing a prosperous future.

The Economic Landscape: Rising Costs and Budgeting

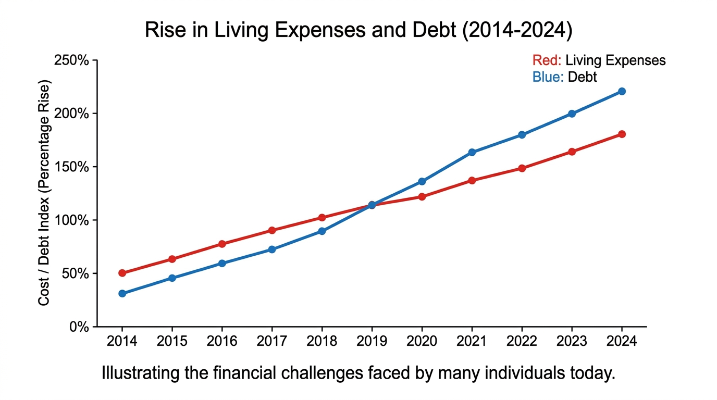

In today’s rapidly evolving economic climate, escalating living costs represent a stark reality for numerous individuals and families. Essentials such as housing, groceries, and healthcare have soared, forcing households to adapt their budgets more stringently than ever. Consequently, many individuals are forced to navigate a precarious financial landscape where monthly expenditures consistently outstrip income. This disturbing trend can lead to a heightened dependence on debt, amplifying financial stress and uncertainty.

Simultaneously, the looming pressure of debt is palpable in the modern economic atmosphere. Student loans, credit card debts, and various other obligations weigh heavily, often resulting in sleepless nights and anxiety. In this context, the ability to manage personal finances has transcended being merely beneficial; it has become essential for survival. Developing effective budgeting skills arms individuals with the necessary tools to track expenses, prioritize essential needs over wants, and reclaim control over their financial circumstances.

Financial literacy and self-discipline are instrumental in achieving individual financial aspirations. By prioritizing personal finance education, individuals can not only alleviate stress derived from living paycheck to paycheck but also establish a solid groundwork for a secure future. This knowledge empowers readers to make informed decisions, reshape financial habits, and foster a secure financial environment. In a world fraught with financial challenges, mastering personal finance should be a paramount objective for everyone.

Step-by-Step Guide on Managing Personal Finances

Effectively managing personal finances is a fundamental aspect of achieving both financial stability and long-term goals. The following step-by-step guide provides practical strategies to enhance money management skills.

1. Track Income and Expenses

The journey of effective financial management begins with meticulous recording of income and expenditures. Begin by outlining all income sources, including salary, bonuses, and supplemental earnings from freelance activities. Then, organize your expenses into two distinct categories: fixed costs (like rent, mortgage, and utilities) and variable expenses (including groceries and entertainment). To streamline this task, consider utilizing financial applications such as Mint or YNAB (You Need A Budget) that automatically sync with your bank accounts, offering real-time updates on financial activity. Alternatively, a well-structured spreadsheet can also visualize your cash flow effectively.

2. Develop a Realistic Monthly Budget

Once you’ve analyzed your tracked income and expenses, the subsequent step is to devise a practical monthly budget. Analyze how much you earn versus how much you spend; this analysis will reveal potential areas requiring adjustment. Aim to follow the 50/30/20 rule: allocate 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. Keep in mind that budgets should not be rigid; they must adapt to accommodate unexpected expenses or changes in income, bolstering financial resilience.

3. Establish an Emergency Fund

Creating an emergency fund acts as a crucial financial safety net against unpredictable events, such as medical emergencies or job loss. Aim to bank three to six months’ worth of expenses. Start with manageable monthly contributions into a designated savings account; consider high-yield savings accounts to augment your interest earnings. This fund will provide a sense of security and prevent reliance on debt during financial strains.

4. Curb Unnecessary Spending

Evaluating spending habits is vital to identify areas where cutbacks are possible. Regularly reexamine your expenses to pinpoint discretionary items that can be diminished or eliminated—think monthly subscriptions or dining out frequently. One effective strategy is implementing a 30-day rule before committing to large purchases, allowing time to assess whether the purchase is essential or a momentary impulse.

5. Strategically Manage and Reduce Debt

Incorporating strategies to manage debt is crucial in safeguarding financial stability. Begin by cataloging all debts, including amounts owed, interest rates, and monthly payments. Consider employing strategies like the debt snowball method (targeting smaller debts for quick victories) or the avalanche method (prioritizing high-interest debts). Consulting a professional may also be beneficial, and it’s vital to avoid accruing more debt by steering clear of impetuous credit card expenditures.

6. Define Short and Long-Term Financial Goals

Establishing financial goals provides direction and motivation to your financial journey. Short-term objectives might include saving for a vacation or upgrading appliances, while long-term goals could relate to retirement planning or homeownership. Break larger goals into actionable steps, implementing deadlines to maintain focus. Adopt the SMART criteria—specific, measurable, achievable, relevant, and time-bound—to further enhance goal clarity.

By systematically applying these steps, you will not only enhance your management of personal finances but also empower yourself to make educated decisions aligned with your financial aims.

Effective Money Management Strategies

To achieve financial stability, several effective strategies can streamline personal finance management. The 50/30/20 Rule remains widely endorsed, allowing individuals to allocate 50% of income to essentials, 30% to desires, and 20% towards savings and debt repayment. This method is celebrated for its simplicity, making it easy to comprehend spending habits. Nonetheless, it may exhibit limitations due to the categorization rigidity, which might not suit all financial circumstances.

Another popular method is Zero-Based Budgeting, which mandates that every dollar earned is assigned a specific role, instilling comprehensive financial awareness. This approach is particularly appealing to those seeking to exercise meticulous control over their spending and maximize savings, although it may demand substantial time investment and thorough tracking of transactions.

Additionally, automating savings plays a critical role in money management. By setting up automatic transfers to savings accounts, individuals can cultivate consistent saving habits while minimizing the temptation to spend first. Utilizing tools like mobile applications and expense tracking systems such as Mint or YNAB can provide insights into spending patterns and help adherents to remain aligned with their financial objectives.

Incorporating these strategies will empower individuals to seize control of their financial health, fostering positive financial management habits.

Real-Life Applications of Personal Financial Management

In the domain of personal finance, divergent approaches resonate with individuals based on their distinct circumstances. For instance, take Lisa, a college student balancing her classes with part-time work. She meticulously tracks her expenses via a budgeting application, categorizing her spending into necessities and leisure. By allocating designated weekly limits to dining and entertainment, she prioritizes experiences while still working towards her financial objectives.

Consider Tom, a young professional navigating the complexities of urban life. Eager to save for a home, he automates his savings, causing a portion of his earnings to funnel directly to a high-yield savings account. This strategy—dubbed “out of sight, out of mind”—has enabled him to amass savings effortlessly, showcasing that scheduling automatic savings transfers can drastically support financial goals.

We also have the Johnson family, attempting to keep their budget balanced amid rising costs. They conduct monthly meetings to reassess their financial priorities. By embracing cost-effective meal planning and hunting for online deals, they’ve discovered ways to save on groceries while preserving quality family meals

Was this helpful? Share your thoughts