Is Long-Term Care Insurance Worth It

Insurance

|

May 18, 2026

"Is long-term care insurance worth it?" This pivotal question resonates deeply for individuals approaching retirement, particularly as healthcare costs continue their upward trajectory. With many grappling with the very real implications of aging, understanding the potential financial risks associated with long-term care needs becomes essential. Without adequate preparation, expenses related to assisted living or nursing home care can severely deplete savings, leading to a daunting financial burden that may come as a surprise to many. Therefore, long-term care planning has assumed a crucial role in protecting one's financial future against unexpected health-related expenditures.

"Is long-term care insurance worth it?" This pivotal question resonates deeply for individuals approaching retirement, particularly as healthcare costs continue their upward trajectory. With many grappling with the very real implications of aging, understanding the potential financial risks associated with long-term care needs becomes essential. Without adequate preparation, expenses related to assisted living or nursing home care can severely deplete savings, leading to a daunting financial burden that may come as a surprise to many. Therefore, long-term care planning has assumed a crucial role in protecting one's financial future against unexpected health-related expenditures.

However, the wisdom of investing in long-term care insurance varies significantly depending on individual situations. Considerations such as financial resources, health history, and personal preferences are fundamental in making this pivotal decision. This comprehensive guide will explore the benefits and challenges of long-term care insurance, outline which demographics stand to benefit most, recommend an appropriate time frame for purchasing such coverage, and identify critical factors to evaluate. Ultimately, our examination seeks to empower readers with the insights necessary to navigate their long-term care planning, ensuring peace of mind during their golden years.

What Is Long-Term Care Insurance?

Long-term care insurance (LTCI) fundamentally serves to cover costs associated with extended care services not typically addressed by standard health insurance or Medicare. It provides significant financial support for individuals needing help with daily tasks due to aging, chronic conditions, or disabilities. By purchasing this insurance, individuals can safeguard their assets and ensure access to required care when independence becomes compromised.

Types of Services Covered

- Nursing Home Care: Detailed around-the-clock medical assistance and personal support in a facility designed for individuals needing extensive help.

- Assisted Living Facilities: Offering a blend of housing and support services, these facilities provide necessary assistance with daily activities while allowing for some degree of independence.

- Home Health Care: Involves professional medical care delivered at home, enabling individuals to receive assistance without leaving their familiar surroundings.

- Adult Day Care Services: Comprehensive programs providing daytime supervision and engagement for seniors or those with disabilities, thereby offering vital relief for family caregivers.

- Care Coordination Services: These services facilitate effective communication and management of care needs between various caregivers and healthcare providers, optimizing the individual's overall care plan.

What Long-Term Care Insurance Typically Does Not Cover

It's essential to note that long-term care insurance often does not include services related to acute medical care, routine check-ups, hospital stays, or most prescription drugs. Additionally, it may exclude coverage related to self-inflicted injuries or pre-existing conditions until certain waiting periods have elapsed.

Differences from Traditional Health Insurance and Medicare

While conventional health insurance primarily focuses on the treatment and management of acute incidents, LTCI specifically emphasizes daily living assistance. On the other hand, Medicare has its limitations concerning long-term care; it primarily covers short-term skilled nursing needs, leaving substantial gaps that LTCI aims to fill, effectively addressing the critical help needed for prolonged assistance scenarios.

In summary, long-term care insurance plays a vital role in bridging discrepancies in traditional insurance coverage, emphasizing the importance of preserving the quality of life for those requiring long-term care support.

Why Do People Buy Long-Term Care Insurance?

Long-term care insurance has emerged as a fundamental component of effective retirement planning for many individuals. Here are several prevalent motivations that drive people to consider acquiring this vital coverage:

Protect Retirement Savings

One of the most pressing reasons for obtaining long-term care insurance is to shield retirement assets. The exorbitant costs associated with long-term care can erode savings rapidly; without adequate insurance, individuals are at risk of decimating their hard-earned retirement funds. LTCI offers a protective buffer, ensuring that individuals can preserve their savings against unexpected medical costs and enjoy a more stable financial future in retirement.

Help Cover Rising Long-Term Care Costs

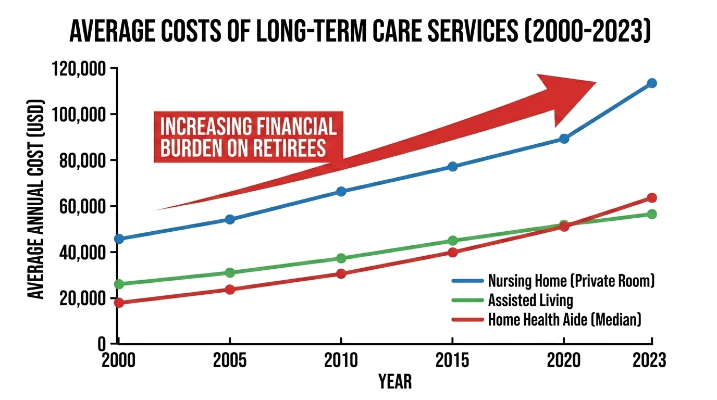

Recent trends have indicated a substantial and persistent increase in long-term care costs. Data shows that expenses associated with nursing homes and home care services frequently outpace general inflation rates. By investing in long-term care insurance early, individuals can strategically prepare for these mounting costs and secure their access to the necessary care without facing overwhelming financial strain.

Reduce Financial Burden on Family Members

A significant motivation behind acquiring long-term care insurance is to relieve the financial pressure placed on family members. In the absence of coverage, families often find themselves in difficult positions, forced to liquidate assets or incur debt to meet a loved one's care requirements. Long-term care insurance helps mitigate these burdens, allowing families to prioritize emotional and practical support instead of facing financial hardships during challenging periods.

Gain Greater Flexibility in Care Choices

Flexibility in determining care options is another notable advantage offered by long-term care insurance. Policyholders can choose to receive care at home, in assisted living, or at skilled nursing facilities, depending on their personal preferences and needs. This means individuals can exert agency over their care experience, as opposed to being limited to options dictated by financial constraints.

Create More Predictability in Retirement Planning

Lastly, long-term care insurance enhances predictability in financial planning for retirement. Knowing that a significant portion of potential healthcare costs is covered enables individuals to strategize their retirement finances more effectively, leading to reduced stress and an improved quality of life as they age.

Pros of Long-Term Care Insurance

Long-term care insurance (LTCI) offers various compelling advantages for individuals and families, particularly concerning retirement planning.

Helps Preserve Personal Assets

A primary advantage of LTCI is its ability to safeguard family wealth. Rising healthcare costs can rapidly deplete personal savings, but LTCI acts as a financial cushion, enabling families to protect their wealth and ensure it remains available for future generations rather than exhausting it on care expenses.

Expands Care Options

With a long-term care insurance policy, individuals gain access to broader care alternatives, providing them the freedom to select the location and type of services that best suit their needs. This variety enhances the person's ability to direct their care in ways that resonate with their circumstances for a more tailored experience.

Provides Coverage Beyond Medicare

Many individuals overlook the limitations imposed by Medicare concerning long-term care. Although Medicare does provide some level of assistance, it typically only covers short-term skilled nursing care or rehabilitation, leading to significant gaps in coverage. LTCI effectively addresses these shortcomings, granting individuals the necessary financial support for their long-term care needs when traditional health insurance falls short.

May Cover Home-Based Care

An increasing number of seniors express a preference for home-based care. LTCI generally caters to this desire by covering in-home services, allowing individuals to receive assistance in familiar and comforting surroundings while retaining their autonomy. This flexibility can contribute to improved emotional health and overall well-being.

Helps Protect Family Caregivers

Moreover, LTCI alleviates the burden placed on family caregivers by providing access to professional support. Knowing that loved ones can receive skilled care reduces stress and anxiety among family members who may otherwise feel overwhelmed by caregiving responsibilities. This assurance fosters healthier relationships and lessens the prevalent burnout frequently experienced by family caregivers.

In essence, long-term care insurance not only fortifies personal assets but also enhances the quality of available care, positioning it as a critical consideration for comprehensive retirement planning.

Cons of Long-Term Care Insurance

While long-term care insurance offers various protections, it is not without notable downsides that families should carefully consider.

Premiums Can Be Expensive

One of the most significant disadvantages associated with LTCI is the financial burden of premiums, which can weigh heavily on families—especially those managing already strained budgets. Recent statistics from the American Association for Long-Term Care Insurance reveal that the average annual premium for a 55-year-old ranges between $2,000 and $3,500. Such sizable costs accumulate swiftly, resulting in a substantial financial obligation.

Rates May Increase Over Time

Additionally, policyholders often find themselves blindsided by escalating rates. Insurance companies reserve the right to adjust premiums based on various factors, including inflation. This can usher in unexpected financial demands in the future, seriously impacting retirement preparations and family finances.

You May Never Use the Benefits

A key consideration lies in the prospect of paying for insurance that might never be utilized. Many individuals may never require long-term care, leaving them at risk for investing thousands into a policy without any returns in terms of claims or services. This possibility evokes critical questions about the tangible value of such insurance coverage.

Coverage Limits and Waiting Periods Apply

Moreover, most standard policies impose coverage limits and require waiting periods before benefits become available, which may create vulnerability when immediate care is needed. Policies often come with stipulations on the types of care that qualify for coverage, leaving beneficiaries responsible for significant out-of-pocket expenses in many instances.

Medical Underwriting Can Be Challenging

Finally, the application process can present hurdles due to medical underwriting. Applicants with pre-existing conditions or health issues may face declines in coverage, thereby leaving them without the financial protection they had anticipated securing. Such uncertainties can prove to be significant barriers for many considering this essential insurance.

Overall, while long-term care insurance promises peace of mind, it is vital to recognize and understand its limitations as part of effective retirement financial planning.

Who Should Consider Long-Term Care Insurance?

Long-term care insurance (LTCI) is a vital component of financial planning, specifically benefiting particular demographics as they near retirement. Here are key groups that may find LTCI especially advantageous:

Middle- and Upper-Middle-Income Households

These demographics frequently possess a stable income yet may find sustained healthcare costs overwhelming. LTCI creates a safety net, ensuring their financial stability remains intact amid unexpected care-related expenditures while allowing them to maintain their lifestyle during retirement.

People With Assets They Want to Protect

For those who have accumulated significant assets—such as homes, savings, or investments—protecting these from potential healthcare costs is essential. LTCI can help preserve these assets from depletion due to nursing home or in-home care expenses, allowing for wealth transfer to heirs.

Individuals Without Reliable Family Caregiving Support

Individuals lacking a strong caregiving network face distinctive challenges as they age. LTCI offers critical resources for care, easing the pressure on family members. This way, individuals can receive the professional assistance they require without overstretching family obligations.

Who May Not Need Long-Term Care Insurance?

Long-term care insurance offers critical benefits, but it is not a blanket necessity for everyone. Several specific scenarios indicate when individuals might forgo this type of coverage.

Individuals With Limited Assets

For those with minimal assets, long-term care insurance may seem less relevant. If an individual possesses modest savings and income, the prospect of long-term care could potentially lead to financial strain rather than providing a safety net. Individuals in this category might prioritize financial products more aligned with their current situations, as premiums for long-term care insurance might be untenable.

Those Likely to Qualify for Medicaid

Individuals expecting to qualify for Medicaid may similarly feel less inclined to invest in long-term care insurance. Medicaid extends substantial coverage for long-term care services, aimed at low-income individuals. By depending on this governmental resource, the financial burden associated with long-term care can be alleviated, rendering private insurance unnecessary.

High-Net-Worth Individuals Who Can Self-Insure

On the other end of the spectrum, high-net-worth individuals typically possess the financial means to self-insure. With ample savings and revenue streams, these individuals can comfortably cover potential long-term care expenses without requiring traditional insurance policies. This practice of self-insurance allows for personalized financial management.

When Is the Best Time to Buy Long-Term Care Insurance?

Investing in long-term care insurance (LTCI) represents a pivotal decision that is optimally made between the ages of 50 and 60. During this window, individuals typically enjoy better health, which translates into a higher likelihood of qualifying for coverage at lower premium rates. Timing is critical, as procrastination can dramatically inflate the costs of securing such coverage.

As individuals age, their premiums inevitably increase due to the heightened risk of health issues. A report from the American Association for Long-Term Care Insurance revealed that the average annual premium for a 55-year-old is $2,058, while it dramatically soars to about $3,600 for a 65-year-old.

Health also significantly affects the consideration of LTCI. Early acquisition benefits individuals, particularly those without pre-existing conditions, as they may overcome eligibility barriers or possible premium hikes.

Delaying the purchase of long-term care insurance can have dire consequences, including facing higher rates or limited options, given that statistically, nearly 70% of individuals aged 65 and older will likely require extensive long-term care. Securing LTCI proactively mitigates financial risks while ensuring peace of mind in retirement planning.

Was this helpful? Share your thoughts