Personal Finance Advice Mastering Your Money for a Secure Future

Finance

|

April 21, 2026

personal finance, money management, financial advice

Managing personal finances has become more challenging as living costs continue to rise and household budgets feel increasingly stretched. Many individuals are dealing with higher expenses, debt pressures, and uncertainty in the job market, making it harder to maintain financial stability. However, with the right strategies, it is still possible to take control of your money and build a healthier financial future. This article explores practical personal finance tips designed to help you budget more effectively, reduce unnecessary spending, and improve long-term financial stability.

What Is Personal Finance Advice?

Personal finance advice encompasses a range of strategies designed to assist individuals in efficiently managing their monetary resources. Acting as a vital compass for the often tumultuous journey of budgeting, investing, and planning for financial goals, it aims to empower people to take informed actions regarding their finances, ultimately enhancing their overall stability and well-being.

The significance of personal finance advice varies across different life stages. Young adults embarking on their careers are often guided to prioritize savings and credit establishment. In contrast, middle-aged individuals may seek counsel on retirement investments, debt management, or funding education for their children. As people transition into retirement, the focus may shift toward income sustainability and healthcare planning. By customizing advice to meet distinct needs, personal finance professionals can foster improved financial habits and mitigate costly mistakes.

In essence, effective personal finance advice not only helps individuals achieve stability but also instills confidence in their financial decisions. Its benefits magnify with age and experience, confirming its status as a lifelong asset for financial growth and health.

Why Personal Finance Advice Matters Today

In a world where the cost of living is continuously rising, the need for astute financial planning has never been more pressing. The soaring prices of essential services—like housing, healthcare, and groceries—mean many individuals and families find their earnings falling short of their basic expense needs. Such financial strain often results in heavy reliance on credit sources, pushing households into cycles of debt that become increasingly hard to escape. Recent studies indicate that over 70% of Americans express anxiety regarding their financial situations, which highlights an urgent need for action.

The impacts of financial strain extend beyond immediate economic concerns; they can affect mental wellness, personal relationships, and overall life satisfaction. When debt weighs heavily on individuals, they may confront challenging decisions that compel them to prioritize short-term necessities over long-range goals, such as saving for retirement or funding educational pursuits.

Thus, as the personal finance landscape grows ever more daunting, achieving financial literacy becomes a crucial skill for tackling these hurdles. Gaining insights into budgeting techniques, effective savings strategies, and optimal debt management can empower household decision-makers and lay the groundwork for a secure financial future. By acquiring the knowledge and tools necessary for sound finance management, individuals can extricate themselves from the clutches of debt and cultivate a resilient economic base that can weather unforeseen challenges.

Core Principles of Effective Personal Finance Advice

Grasping the core tenets of personal finance is vital for attaining financial independence and stability. Here are five foundational principles to navigate:

- Spend Less Than You Earn: This is the bedrock of financial health. Ensuring that your outlay does not exceed your income creates a buffer for savings and investments. For example, if you bring home $3,000 monthly, aim to cap your expenses at $2,500. The excess can be funneled into either savings or debt repayment.

- Build Emergency Savings: The unpredictability of life necessitates the establishment of an emergency fund. Striving for a fund that covers three to six months of living costs will provide financial peace amidst unexpected crises. If your monthly expenses tally $2,000, target a savings cushion of at least $6,000.

- Track All Expenses: Detailed expense tracking allows insights into spending patterns, helping individuals recognize where they can economize. Employ budgeting apps or spreadsheets to classify and analyze expenses. For example, identifying an excessive dining-out budget can prompt adjustments to save more effectively.

- Avoid Unnecessary Debt: While some level of debt is often unavoidable, especially regarding significant investments like a home, it is crucial to steer clear of high-interest debts, such as credit card balances. If debt is accumulated, prioritize repayment to minimize compounding interest costs.

- Set Financial Goals: Formulating both short- and long-term financial objectives brings clarity to budgeting efforts. Whether accumulating savings for a vacation or preparing for retirement, defined goals can motivate adherence to financial plans. For instance, aiming to set aside $5,000 for a much-anticipated vacation can strengthen budgeting discipline.

Implementing these principles establishes a robust financial foundation that fosters better navigation through the complexities of personal finance, enhancing overall financial health and satisfaction.

Practical Personal Finance Advice for Everyday Life

Navigating personal finance on a day-to-day basis lays the groundwork for long-term economic security. Following these actionable tips can streamline your financial management:

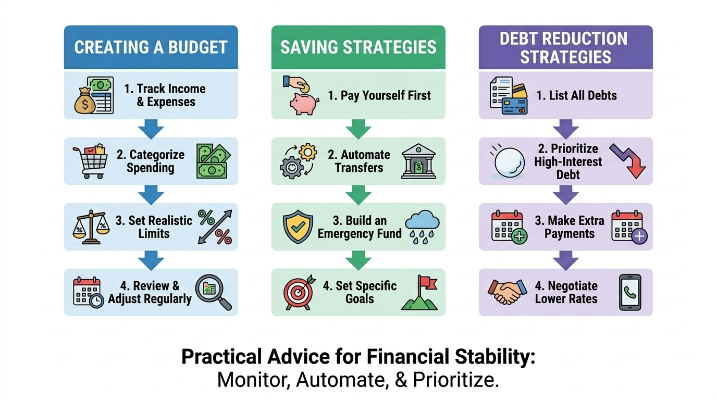

1. Monthly Budgeting: Initiate by diligently tracking your income and expenditures for at least a month. Make use of budgeting tools or spreadsheets to segment expenses into fixed (rent, utilities) and variable (entertainment, groceries) categories. Deviating from the common model, aim to distribute your income with 50% allocated to needs, 30% to wants, and 20% to savings, adjusting these ratios to suit your financial context.

2. Smart Saving Techniques: Create an automated savings system by designating a specific amount for monthly transfer to a savings account. Investigate high-yield savings accounts or certificates of deposit (CDs) aimed at maximizing your interest earnings. Additionally, establishing an emergency fund that embodies 3-6 months of expenses can act as significant financial insulation against unpredictable life events.

3. Debt Reduction Strategies: Should you find yourself in debt, outline a repayment strategy using techniques like the snowball or avalanche method. The snowball approach focuses on first clearing the smallest debts to build momentum, while the avalanche method concentrates on eliminating the highest-interest debt to save on accruing interest over time. Whenever feasible, making payments above the minimum will chip away at both principal and interest.

4. Expense Prioritization: Periodically audit your spending habits to find feasible reductions. Identify essential expenses versus discretionary spending, and consider creating a “cooling-off” period for non-essential purchases using the 24-hour rule, which allows for recalibration before impulse spending occurs.

Incorporating these practical insights can greatly enhance financial wellness, granting greater dominion over your finances and setting the groundwork for a more secure future.

Common Financial Mistakes to Avoid

Navigating the landscape of personal finance also means evading frequent pitfalls that could jeopardize financial security. One prevalent error to note is neglecting small recurring expenses. While it may seem trivial, these costs can aggregate and exert pressure on your total budget. Regularly evaluating subscriptions and other periodic costs can reveal unnecessary charges.

Another common misstep is overspending beyond one’s means. The allure of lifestyle inflation may lead individuals to overspend when earnings rise. To prevent this, it’s critical to formulate a budget emphasizing savings while resisting the impulse to increase outlays.

Failing to maintain an emergency fund can also expose households to surprise expenses that may necessitate credit reliance. Setting aside an amount representing three to six months of essential living costs into a separate savings pool will fortify your financial resilience.

Lastly, an overreliance on credit can entrap individuals in a debt cycle. To counter this, balance your expenditures with prudent savings, leverage credit responsibly, and ensure that charged amounts can be paid off in full each month. Acknowledging these prevalent mistakes, along with actionable measures to evade them, can vastly reinforce your financial stability and empower sound decision-making for the future.

Real-Life Applications of Personal Finance Advice

The application of proficient personal finance advice is pivotal across different life stages. Here's how various groups can apply financial strategies:

For Students: Managing finances while pursuing academic priorities can feel overwhelming. One crucial initiative is establishing a detailed monthly budget that accounts for tuition, living expenses, and discretionary spending. Utilizing budgeting apps, such as Mint, can simplify tracking expenses and minimize risk of overspending. Students may also explore student discounts and part-time employment opportunities to accumulate income sources.

For Young Professionals: Following graduation, young adults must prioritize establishing a robust credit score. This can be achieved through timely repayment of credit card balances and circumscribing credit usage. Additionally, even modest contributions to a retirement plan can foster long-term wealth appreciation through compound interest. Engaging in employer-sponsored plans or opening a Roth IRA are effective starting steps.

For Families: As families grow, budgeting becomes exponentially more significant. Utilizing the ‘50/30/20 budgeting rule—where 50% goes to needs, 30% to wants, and 20% to savings or debt repayment—can streamline distribution and enhance financial allocation. Families should also house an emergency fund with at least 3-6 months’ worth of expenses.

For Freelancers: With unpredictable income flows, financial discipline is vital for freelancers. Establishing a distinct business bank account helps in segregating income and expenditures. Drafting contracts that stipulate payment terms can provide protection against late payments, ensuring financial steadiness.

By customizing financial advice to the unique contexts of each group, individuals can swiftly transition from awareness to action, paving a road toward a secure and prosperous financial future.

Was this helpful? Share your thoughts